Have you started your home savings account and aren’t what to do with the funds? Do you feel like you’re not doing enough with that down payment fund and wonder what move is the best one? Let contributor Andy Shuler’s home buying story inspire you and give you wisdom on what to do.

BACKSTORY: Less than a year ago, my wife and I found ourselves in a situation where we were moving to a new city and were in the housing market. I was expecting to move in March of 2019, but was offered a really good, new opportunity in late October that I couldn’t pass down.

While both my wife and I were excited about moving and the excitement that going to a new place brings, I was also extremely stressed out about money.

You see, in my eyes, I was operating under the assumption

that we weren’t going to move until March.

I thought I still have 4-5 more months of saving and really increasing

the amount that we could put down on a house.

It turns out that we didn’t have that time, so we had to make do as best

as we could.

Luckily, we had been financially planning for a move for

quite some time, knowing that my company will typically move employees every

2-3 years, so we were planning for the next move before we even unpacked our boxes

in Chicago.

This was the first time that we were buying a house instead

of renting, and really had absolutely no idea where to begin.

I spent countless hours (like easily in double digits)

researching all of the different types of down payment options to make sure

that we found the best way to maximize our home savings by making sure that we

selected the right down payment option.

Like I mentioned, we had been planning to buy a house for a

good while. While living in Chicago, we

got engaged and married, both of which are extremely expensive, to get a ring

and to pay for a wedding. We also, as I

mentioned, were living in Chicago, which is expensive in itself.

So, while we had been saving for a while, it wasn’t a

shoe-in that we were just going to put 20% down. I really spent a lot of time budgeting,

saving, and researching to make sure we were optimizing our home savings.

First off, once extra money was leftover from the budget,

that all went into our “down payment fund.”

But what should we do with that money that’s saved for our next home?

Home Savings Option 1: Fifth Third savings account with .01% interest

I don’t feel bad putting Fifth Third on blast about this because they deserve it. Actually, I feel as bad about calling them out by name as they do by only giving .01% interest – not at all.

If I put $350 into the savings account every paycheck since moving to Chicago and took it out on the day that we closed on our new house, that $19,250 would be worth $19,252.

Wow. I actually laughed out loud when I ran this math.

Home Savings Option 2: Invest it in the stock market

I was really just getting into investing in Chicago and I sooo wanted to do this. I even convinced myself that I could just put it in the Roth IRA since you can take it out for first-time home buyers using it on a down payment on a house. I am ecstatic that I didn’t.

This is where I am so incredibly happy that I did research and learned that if you’re investing only in the short-term, the stock market can be very volatile and is likely not a good idea.

If I put $350 into the S&P 500 every paycheck since moving to Chicago and took it out on the day that we closed on our new house, the $19,250 that was put in would be worth $18,546, or a loss of $704. Ouch.

Home Savings Option 3: Open a high-interest savings account

This is what we chose to do. It seemed like a good combination of both options. It was no risk for a decent return, and a guaranteed return at that.

In total, if we chose to put in $350 into the savings account every paycheck since moving to Chicago and took it out on the day that we closed on our new house, that $19,250 would be worth $19,696.

Overall, a small increase of only $446, but that’s $444 over the next best alternative.

Very happy this is the decision that we made.

Now that we decided on the method to save, the next topic

was what were we saving for? What sort

of down payment could we handle? I

looked into tons of options and narrowed it down to the ones that stuck out

most to me:

Mortgage Option 1: Put 20% down (or more)

This likely seems obvious, but this is always the preferred option. Not only does putting 20% down allow you to have lower monthly payments, but most importantly, it keeps you from having to pay Private Mortgage Insurance (PMI).

PMI is essentially an insurance to the lending company in case you default on the mortgage.

Because you’re paying 20% or more of the house value upfront, the risk that you will default is much less than if you were putting less than 20%, so you get to avoid PMI and trust me, you really want to avoid PMI.

Mortgage Option 2: Piggyback Loan (80-10-10) – 10% Down

I view this as 1B to paying 20% down. A piggyback loan where you take out a mortgage for 80% of the home value, take out a second mortgage for 10% of the loan, and then put 10% down.

This is one of the options that we really strongly considered.

The offer that was extended to us was 3.5% APR on the first mortgage for 80% that lasted 30 years, 5.5% on the second mortgage for 10% of the loan that lasted 10 years, and then putting 10% down.

The major pro of this loan is that it allows you to not have to pay PMI while not putting down 20% for the down payment.

The major con though is that for the first 0 years, you’re going to have much higher payments because you’re paying that second mortgage at a higher interest rate.

This type of loan is not very common, but I think it’s truly a diamond in the rough when used properly.

The key is to not overextend your means with that second mortgage, but it can really come in handy for those that might have a good salary but haven’t saved up enough for one reason or another.

Mortgage Option 3: Conventional Loan with 10% Down Payment

This loan is simply just putting down 10% and taking out a 30-year mortgage on the remaining 90% of the home value.

Overall, this option isn’t the worst thing you can do as long as you can afford the payment and should anticipate paying PMI at least until you get 10% of the principal paid off in addition to the down payment.

There are other options, such as a Rural Housing Loan (USDA Loan), FHA Loan, Conventional 97/3, etc., that all offer a lot of benefits on their own, but these weren’t loans that we qualified for or really entertained, because of the lower down payment.

In general, I know a lot of people use 20% as a threshold for a down payment, but I fall more in the 10% camp, so I wanted to focus on that as a floor.

All in all, I highly recommend option 1 (20% down) and

option 2 (piggyback loan). In my

opinion, avoiding PMI is an absolute must.

PMI can really set you back as you’re paying a lot of extra money each

month just because you’re a higher risk to the lender.

Many people will simply think “I’m paying $900/month now for

rent, I can get a house with a $900 mortgage too.” That sounds great in theory, until your AC

breaks, you need a lawn mower, your home floods, etc…and you have to pay for

100% of that, compared to 0% when you’re renting. I

n our first few months of homeowning, we’ve had to replace

our driveway and our AC…and the other charges didn’t stop, like the need to get

new tires on one of our cars.

Please, save up enough to avoid PMI. You’ll be happy you did.

Let me prove it to you.

I found a calculator online at https://www.hsh.com/calc-pmi.html and

it allowed me to project loan payments with PMI, so I took a look at some

different situations. Let’s look at one

specific example:

Assumptions

Your credit score – Fair (700-719)

Interest Rate – 3.5%

30-year mortgage term

$200,000 home value

20% Down ($40,000)

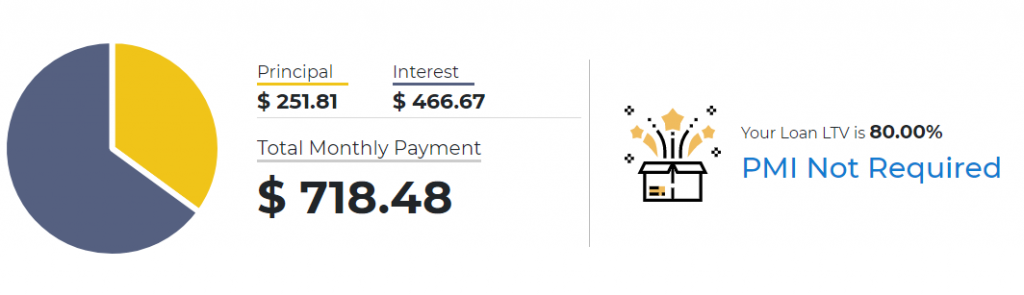

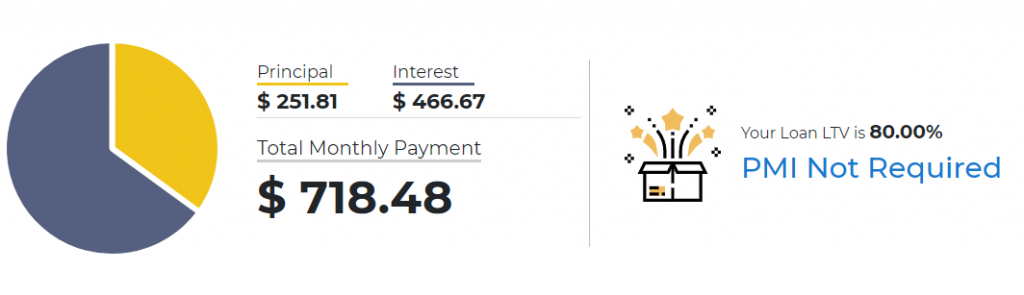

Entire Mortgage

Loan – $160,000 (80% of $200,000)

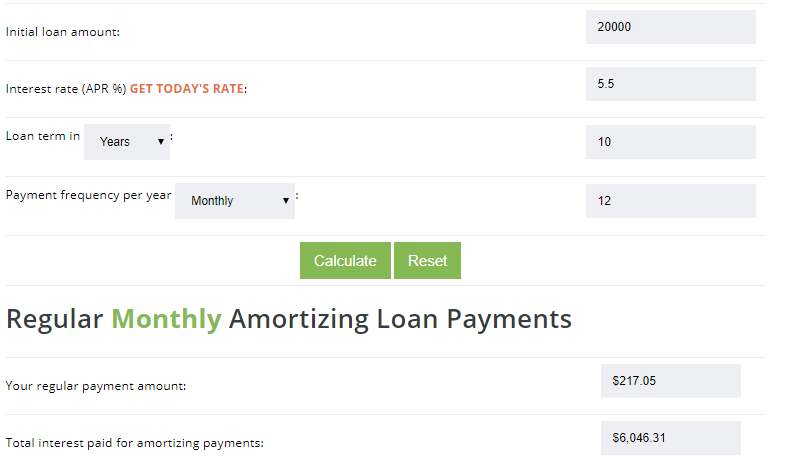

Piggyback Loan (80-10-10) – 10% Down ($20,000)

First Mortgage Loan – $160,000 (80% of $200,000)

Second Mortgage Loan

– $20,000 (10% of $200,000) Note that I’m also

assuming the interest rate is 2% higher than the 1st mortgage, which

is common for this type of loan, and that it’s a 10-year payoff period.

In summary, your total payments would look like this for the

three loans:

As you can see, your payments are considerably cheaper each month if you put down 20%, as well as that you avoid PMI.

This is why putting down 20% is always the #1 best choice, without a doubt.

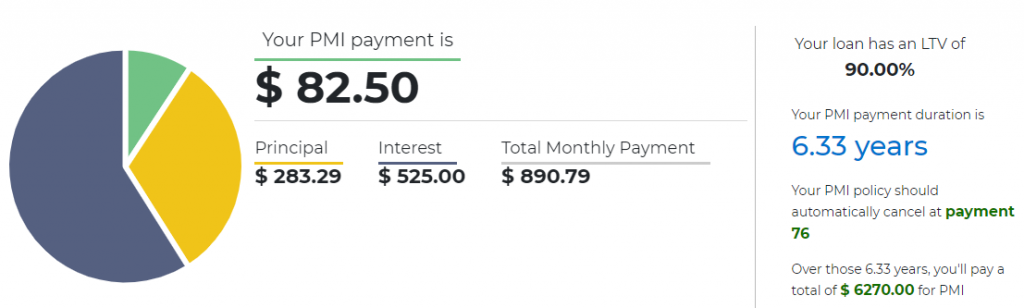

The next best choice might seem like the 10% down option, but I disagree. With the 10% loan, you’ll notice that you’re paying $82.50/month in PMI, which is just being flushed down the drain vs. $0 PMI with the Piggyback loan.

Think of this as buying in bulk – the upfront cost of buying something in bulk is obviously more, but it might be less on a cost/item basis.

This is very similar here. You’re going to pay $45 more per month with the Piggyback, but that’s all going towards the principal and house interest, instead of being wasted on PMI.

So, what is the best loan to go with?

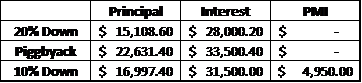

Let’s fast-forward 5 years and see how much you would’ve

paid in Principal, Interest and PMI with each of these loans:

Now the Piggyback loan might seem like a better option,

right? You’ve paid that extra $45/month,

or a total of $2700 in 5 years, but your Principal is $5,634 more paid off then

the simple 10% down loan, and that’s because you’ve paid $4,950 in PMI with the

10% down loan.

So, if you went with just paying 10% down, you’ve paid

$2,700 less over those 5 years, but your house has $5,634 less paid off than

the alternative – not ideal.

All in, let’s take a look at the total “wasted money”, which

is the Interest + PMI:

As you can see, there is a clear loser here…

If you only take away one thing from this article, it’s to make sure that your home savings is enough to avoid PMI. I normally hear people say to make sure you have 20% down, but I don’t 100% agree with that.

In my opinion, the best part of 20% down is to avoid PMI, and you can do that with only putting down 10% as well, but you have to be smart and disciplined about it.

Just as I did, take some time to research, crunch your own

numbers, and save up enough money so that you’re making the best decision for

you. Good luck in your house-buying

journey!

The post Optimizing Home Savings with the Right Down Payment Options appeared first on Investing for Beginners 101.

The Transparent Traders Blackbox 💸 Amazingly simple!

What’s in the box?

Our Blackbox is the first-ever to be created that specifically alerts for swing trades. It will also alert for bullish & bearish day trades.

The Blackbox runs off of multiple algorithms and uses predictive A.I. to locate the most accurate day or swing trades that it calculates to give the best chance for success.

Transparent Traders

Private group · 6,900 members

Join Group

Transparent Traders exists to solve the critical issues facing our traders, both large and small. Our unique approach is not only what differentiates ...

Contact Us: We Can Help the Trading Community Learn About Your Company or Product.

Post a Comment