Have you ever thought it’d be nice to have an Excel formula to calculate the CAGR on your investments that move more unpredictably rather than in a perfectly straight line? Contributor Andy Shuler has just created a new CAGR formula Excel spreadsheet to help investors plan their future—even when things don’t go exactly according to plan.

If you’re an absolute beginner, Andy’s written a great intro into everything about CAGR and why you’d want to calculate it as an investor.

If you’re just looking for the Excel CAGR formula, then go ahead and scroll down to where the big colorful pictures are (and be sure to download the tool for free for yourself!).

Introduction to Compounding and CAGR

CAGR. What the heck

is CAGR? Well, it’s an acronym for

Compound Annual Growth Rate, or in other words, it’s the rate that something

compounds on an annual basis. Almost

always, this will be in reference to money, but that’s not the only time this

applies. Let’s get down to some Compounding

101…

You might’ve heard people say, “I compounded the

problem by trying to make things right.”

What they are actually saying is that they took a bad situation and made

that situation even worse. Fortunately

for all of us, not all examples of compounding are about making situations

worse.

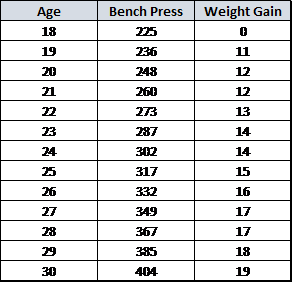

For instance, imagine if you were a bodybuilder and you were

told that from ages 18-30 you would gain 5% in your bench press each year. If you benched 225 pounds as an 18-year-old,

your next year you’re going to bench 236 pounds (1.05*225), or an increase in

11 pounds. The next year you would bench

248 pounds (1.05*236), or an increase in 12 pounds. In essence, you will gain more strength each

year because you’re gaining 5% strength on a larger number.

As you can see by looking at the

chart above, you will have gained 19 pounds in strength when you’re 30

(385*1.05) compared to the 11 pound gain your first year. This, in essence, is the beauty of compound

interest.

The longer that you let something

have the ability to compound, the larger your number in the end will be,

because you’re building on top of those gains (both literally (GET SWOLL!) and

numerically).

Please note that this is an

example and not me saying you’re going to go from benching 225 to 400+ in 12

years, although I’m sure some people do, and I can confirm that I am not one of

those people. Something that’s very

important to note, both in this example and in any other, is that our bodies

don’t continue to get in better shape, and eventually we will likely experience

health issues, so the value of compounding mainly comes from time.

The sooner you start, the better,

because you will have that much more time to allow your task to compound.

Applying CAGR to Money in the Stock

Market

Now, to put this into money

terms. The same exact philosophy can be

applied towards investing.

The earlier that you start

investing, the earlier that you will start seeing the benefits of investing in

the stock market, and the larger that those benefits will be when you get to retirement

age. Want to have your mind blown? Ok, FINE!

I’ll do it – you twisted my arm…

If you invested $100/month for your child starting the month they were born and you received an 8% CAGR (the S&P 500 average since 1950 is 11%), then you would have $1,778,852.75 when they turned 60, which would’ve cost you a total of $72,000 ($100*12 months*60 years).

For your child to have about that same amount of money when they turned 60, assuming they started investing when they were 22 and also received an 8% CAGR, they would have to invest over $602/ month for 38 years. Doing this would’ve cost them a total of $274,512 ($602*12 months*38 years)! How insane is that.

That, my friends, is the value of

compound interest.

Time matters more than the actual

amount that you put in. By starting when

your child was just born, you can have the same amount for them when they’re 60

by putting in $200,000 less in total (You put in $72,000 in total while they

put in $274,512 in total).

Now, I’ll admit, this might seem like

a somewhat outlandish type of comparison because you are likely looking for how

to get your own retirement going, and I 100% respect that.

I am in that same boat.

You need to focus on yourself

first, because if all you do is save for your child, then they’re going to be

paying for your retirement (so it basically is you saving for it in a

roundabout way lol). But I challenge you to really, really think about this…

If your goal is to live a happy

life, and you want your children to live a great life, then can you find

$100/month that you’re blowing on something you don’t need? The cost is so

small to you to set them up for success in their life.

Maybe it’s not $100.

Maybe it’s $25. That’s literally

one meal for yourself and your spouse.

Can you eat at home one extra night/month?

Saving $25/month for that same 60 years will give them $444,713.19… not nearly as high as $100 / month, but still enough to make a significant difference in their quality of life. Ok, end rant.

So, you likely understand the value

of compound interest now, and that while the amount that you put in is

important, time is the most important factor, so it’s better to start as early

as possible.

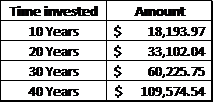

A couple months ago I wrote an article that showed you how to calculate compound interest based on a static number, for instance, if you inputted $10,000 dollars and you let it earn X interest for X years, how much would you have?

Such as, if you invested $10,000

into the stock market and realized a 6% CAGR (reminder that the S&P Average

since 1950 is 11%), you would have the following:

I’ve found some great compound

interest calculators online that are very helpful, but they’re basic and

somewhat inflexible. I wanted to create

something that you could use that really fits the situation that you’re

in.

For instance, maybe you intend to

invest $250/month each and every month.

That’s great! But, what if your

AC dies on you (like ours just did) and you now have the choice – die of heat

exhaustion and go without AC, or slow down your investing a bit?

I know there’s always more

options, but for this sake, let’s assume that you decide to do a combination of

spending less and investing less to help you pay for the AC, and you will have

to go three months without investing for retirement.

Well, my Excel CAGR Formula toolcan calculate that, and online calculators cannot. Let’s take a look!

Andy’s CAGR Formula (Excel) Explained

On the tab labeled ‘Contribution

Details’ you can input how much money you plan to invest and how much you have

actually invested. You’ll notice that the

first 7 months are green, but that’s just because I like to highlight finalized

numbers, so I know what’s planned and what is an actual. All of these cells are hardcoded, so you can

simply go in and change your anticipated savings amount for any month by just

overwriting the cell. It’s a very easy

update to make!

Click to Zoom

Step 2 is to take a look at the

tab titled ‘CAGR Calculator’. All you

need to do is change the cell that’s highlighted green to update what

assumption you want to make for your portfolio growth. Once you do that, the rest auto-populates

based on your input on the previous tab.

Click to Zoom

My favorite thing about this tab

is that it’s able to be personalized.

You can manually update your investment amounts each month because guess

what, life happens – you’re not always going to invest the exact same amount

each month from now until death. Not

only that, but maybe you want to update your portfolio with actual data!

For instance, let’s imagine that

you get huge returns your first year and now instead of your portfolio sitting

at $2342, which would be your expected amount based off the returns that I

inputted (8%) and the monthly investments that I added, your portfolio is

sitting at $3300! Talk about a monster

year.

To update this, all you need to

do is simply override the cell. So,

since we’re saying you ended the year at $3300 in this hypothetical example,

update the December 2019 cell to $3300 and then it will continue calculating

the remaining years based off that same value.

Click to Zoom

Now, that’s all lovey dovey and a

good problem to have… “oh, I made too much money, how am I ever going to update

my spreadsheet” Wah wah, boo hoo.

The best part of this CAGR

Calculator Excel version is that instead of you seeing 8% returns year 1, your returns

are pathetic! Let’s pretend you end the

year at $2195, or a -5% return! Dang,

that was brutal. BUT! This tool can show you what you need to do to

get back on track.

For instance, in our first

example of 8% returns, your total portfolio would be $9231 after three years:

Click to Zoom

But, we just discussed that your

Year 1 return was very low, so you need to make that up somehow. So, how do you do that? Well, your first you need to input your

actual Year 1 return in the December 2019 cell, which was $2195.

Next, go to the ‘Contribution

Details’ tab and change your Contribution Amount for the months that you think

you can. If you changed your contribution amount each month for Years 2 & 3

from $250 to $257, you’re actually ahead of the $9231 goal that you initially

had, see below:

Click to Zoom

I really urge you to play around with this tool, use it however best benefits you, and let me know directly if you have any feedback that I can consider to make it better and build out other tools with.

I think this has a great ability to be flexible when you’re looking at retirement, because let’s be honest, getting to retirement requires more flexibility than a yoga class.

The post A Flexible CAGR Formula Excel Tool for Planning Your Chaotic Life appeared first on Investing for Beginners 101.

The Transparent Traders Blackbox 💸 Amazingly simple!

What’s in the box?

Our Blackbox is the first-ever to be created that specifically alerts for swing trades. It will also alert for bullish & bearish day trades.

The Blackbox runs off of multiple algorithms and uses predictive A.I. to locate the most accurate day or swing trades that it calculates to give the best chance for success.

Transparent Traders

Private group · 6,900 members

Join Group

Transparent Traders exists to solve the critical issues facing our traders, both large and small. Our unique approach is not only what differentiates ...

Contact Us: We Can Help the Trading Community Learn About Your Company or Product.

Post a Comment